Economic Management & Global Business Studies invites you to contribute to the frontier of knowledge across disciplines and share your research with a global audience of peers and enthusiasts alike

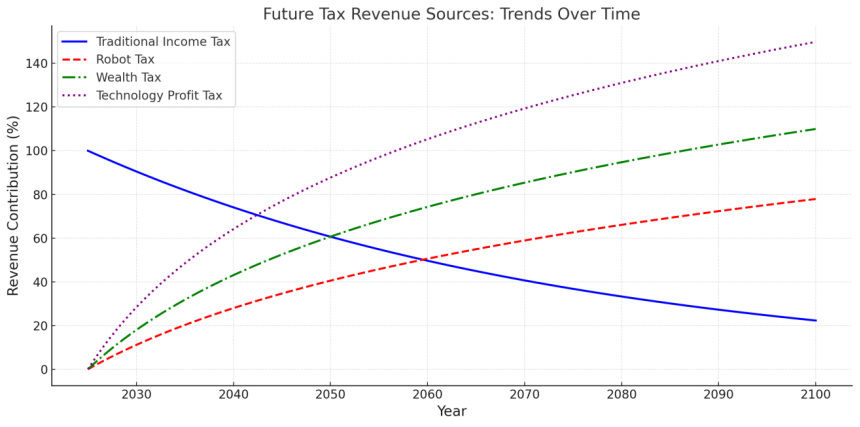

This paper delves into the distinctions between China's and the United States' tax systems, underscoring the pressing requirement for tax reform in China. It scrutinizes the potential of these reforms to propel the evolution of social civilization, emphasizing equity, efficiency, and the digital metamorphosis of tax governance.

Introduction: The tax systems of China and the United States are divergent, mirroring their economic frameworks and policy priorities. The U.S. tax system prioritizes direct taxes, focusing on individual taxation and income redistribution. Conversely, China's system, with its emphasis on indirect taxes, is predominantly geared towards fiscal revenue collection from businesses. This comparative analysis unveils the imperative for China's tax system to adapt in accordance with global benchmarks and the burgeoning digital economy, and imagines the future of taxation in the coming eras

Chen, B. (2024). The Imperative Need for Tax Reform in China and Its Impact on Advancing Social Civilization. Economic Management & Global Business Studies, 3(1), 16. doi:10.69610/j.emgbs.202412311

ACS Style

Chen, B. The Imperative Need for Tax Reform in China and Its Impact on Advancing Social Civilization. Economic Management & Global Business Studies, 2024, 3, 16. doi:10.69610/j.emgbs.202412311

AMA Style

Chen B.. The Imperative Need for Tax Reform in China and Its Impact on Advancing Social Civilization. Economic Management & Global Business Studies; 2024, 3(1):16. doi:10.69610/j.emgbs.202412311

Chicago/Turabian Style

Chen, Bing 2024. "The Imperative Need for Tax Reform in China and Its Impact on Advancing Social Civilization" Economic Management & Global Business Studies 3, no.1:16. doi:10.69610/j.emgbs.202412311

Chen, B. The Imperative Need for Tax Reform in China and Its Impact on Advancing Social Civilization. Economic Management & Global Business Studies, 2024, 3, 16. doi:10.69610/j.emgbs.202412311

AMA Style

Chen B.. The Imperative Need for Tax Reform in China and Its Impact on Advancing Social Civilization. Economic Management & Global Business Studies; 2024, 3(1):16. doi:10.69610/j.emgbs.202412311

Chicago/Turabian Style

Chen, Bing 2024. "The Imperative Need for Tax Reform in China and Its Impact on Advancing Social Civilization" Economic Management & Global Business Studies 3, no.1:16. doi:10.69610/j.emgbs.202412311

APA style

Chen, B. (2024). The Imperative Need for Tax Reform in China and Its Impact on Advancing Social Civilization. Economic Management & Global Business Studies, 3(1), 16. doi:10.69610/j.emgbs.202412311

Article Metrics

Article Access Statistics

References

"Historical Federal Individual Income Tax Rates & Brackets, 1862-2021", Tax Foundation, August 24, 2021.

"Individual Income Tax Law of the People's Republic of China", on www.npc.gov.cn, December 20, 2024.

Sino-U.S. Tax System and Tax Burden Comparison (2023)", Tencent News, November 29, 2023.

“Comparing the Corporate Tax Systems in the United States and China” by Erica York, Alex Durante, Alex Muresianu on May 3,2022 on Tax Foundation (https://taxfoundation.org/research/all federal/us-china-competition-corporate-tax/)

"Taxing Artificial Intelligence and Robots: Critical Assessment of Potential Policy Solutions and Recommendation for Alternative Approaches", IBFD, September 9, 2021.

"Digital taxation, artificial intelligence and Tax Administration 3.0: improving tax compliance behavior - a systematic literature review using textometry (2016-2023)", published on Accounting Research Journal (ISSN: 1030-9616)

OECD Economic Outlook, Interim Report September 2024

“Shifting the balance from direct to indirect taxes: bringing new challenges” on Tax policy and administration - Global perspectives June 2013 from PwC official website.

“Tax Policy Reforms 2024” on OECD and Selected Partner Economies published on September 30, 2024.

“International Tax Competitiveness Index 2024” by Alex Mengden, Tax Foundation, on October 21, 2024.

“A comparative study on the environmental and economic effects of a resource tax and carbon tax in China: Analysis based on the computable general equilibrium model” on ScienceDirect 2021

“Social security reforms, capital accumulation, and welfare: A notional defined contribution system vs a modified PAYG system”Published on 24 February 2024 ,Volume 37, article number 27, (2024)

“The Role of Artificial Intelligence In Tax Administration And Compliance: A New Era of Digital Taxation” published on May 7,2024 by Shalini Aggarwal (DOI: https://doi.org/10.53555/kuey.v30i1.7581)

“Tax transformation: Adopting AI to drive efficiencies” by Randy Carpenter (EY partner) & Daren Campell on July 22, 2024 on 2023 EY Tax and Finance Operations survey

PwC China's '2023 China Tax Policy Review and 2024 Outlook

“Artificial Super Intelligence(ASI) in Tax Administration: Role and Limitations” issued by Hong Zhigang & Chen Yiming from New Rights Journal, Volume 2, 2024