Economic Management & Global Business Studies invites you to contribute to the frontier of knowledge across disciplines and share your research with a global audience of peers and enthusiasts alike

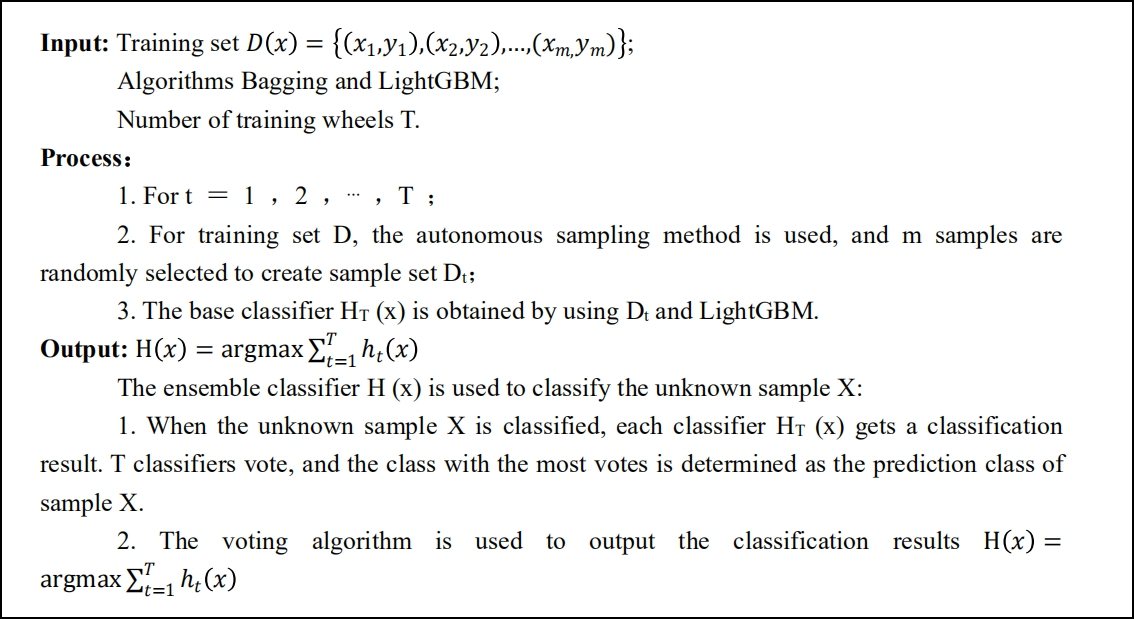

P2P (Peer to Peer) online lending is an emerging Internet finance mode that gathers small-amount fund lending to fund demander. This paper draws on the existing credit risk assessment research, combines rationality, science and other principles, according to the characteristics of the famous online loan platform, collects borrower information and combines computer technology to design a borrower credit risk assessment system. In this paper, we make improvements based on the famous LightGBM algorithm (Light Gradient Boosting Machine). Firstly, In the process of data input, the improved Convolutional Neural Network CNN model is adopted to extract features from the data. Specifically, the Global Average Pooling(GAP) layer is adopted to replace the full connection layer to improve the Convolutional Neural Network. This paper first proposes a P2P online loan default prediction model based on GCNN-LightgBM. The model integrates the advantages of the improved Convolutional Neural Network and LightGBM model, and realizes the efficient prediction of network loan default. Then, in order to improve the accuracy of P2P online loan borrower default prediction, this paper proposes a new model based on LightGBM and Bagging (LGB-BAG). LGB-BAG uses LightGBM as the base learner. With the help of LightGBM, which can effectively reduce the deviation of the model, and Bagging, which can reduce the variance of the model, the volatility of the prediction is further reduced (F1 variance), so that the LGB-BAG model has smaller deviation and variance, and the prediction effect is further improved. In our ablation experiment, the proposed model (GCNN-LGB-BAG) obtained an AUC of 0.86 and an accuracy of 0.97, both of which outperformed all benchmark models. This paper uses actual data to identify the loan risks of P2P online lending platforms, aiming to provide investment reference for investors and methodological support for relevant online lending regulators.

Zainal, L. B., & Al-Masri, A. (2023). An Information Processing and Decision Support model for Credit Default Prediction in Emerging Internet Finance Markets. Economic Management & Global Business Studies, 2(1), 5. doi:10.xxxx/xxxxxx

ACS Style

Zainal, L. B.; Al-Masri, A. An Information Processing and Decision Support model for Credit Default Prediction in Emerging Internet Finance Markets. Economic Management & Global Business Studies, 2023, 2, 5. doi:10.xxxx/xxxxxx

AMA Style

Zainal L. B., Al-Masri A.. An Information Processing and Decision Support model for Credit Default Prediction in Emerging Internet Finance Markets. Economic Management & Global Business Studies; 2023, 2(1):5. doi:10.xxxx/xxxxxx

Chicago/Turabian Style

Zainal, Latifa B.; Al-Masri, Arijit 2023. "An Information Processing and Decision Support model for Credit Default Prediction in Emerging Internet Finance Markets" Economic Management & Global Business Studies 2, no.1:5. doi:10.xxxx/xxxxxx

Zainal, L. B.; Al-Masri, A. An Information Processing and Decision Support model for Credit Default Prediction in Emerging Internet Finance Markets. Economic Management & Global Business Studies, 2023, 2, 5. doi:10.xxxx/xxxxxx

AMA Style

Zainal L. B., Al-Masri A.. An Information Processing and Decision Support model for Credit Default Prediction in Emerging Internet Finance Markets. Economic Management & Global Business Studies; 2023, 2(1):5. doi:10.xxxx/xxxxxx

Chicago/Turabian Style

Zainal, Latifa B.; Al-Masri, Arijit 2023. "An Information Processing and Decision Support model for Credit Default Prediction in Emerging Internet Finance Markets" Economic Management & Global Business Studies 2, no.1:5. doi:10.xxxx/xxxxxx

APA style

Zainal, L. B., & Al-Masri, A. (2023). An Information Processing and Decision Support model for Credit Default Prediction in Emerging Internet Finance Markets. Economic Management & Global Business Studies, 2(1), 5. doi:10.xxxx/xxxxxx

Article Metrics

Article Access Statistics

References

[1]POPE D G ,SYDNOR J R .What’s in a picture ?Evidence of discrimination from prosper [J].Journal of Human Resources ,2011 ,46(1) :53-92.

[2]RAVINA E .Love & loans :the effect of beauty and personal characteristics in credit markets [J]. SSRN Electronic Journal ,2012. DOI :10 .2139/ssrn .1107307 .

[3]Lai Hui, Shuai Li, ZHOU Zheng Fang. A new method of credit Evaluation for personal credit customers [J]. Technical and economic ,2014 ,33(9) :97-103.

[4]Herzenstein, Michal, Sonenshein, Scott, Dholakia, Utpal M. Tell Me a Good Story and I May Lend You Money: The Role of Narratives in Peer-to-Peer Lending Decisions[J]. Journal of Marketing Research, 2011, 48(SPL):S138.

[5]Michels J . Do Unverifiable Disclosures Matter? Evidence from Peer-to-Peer Lending[J]. Accounting Review, 2012, 87(4):1385-1413

[6]Stein J C. Information Production and Capital Allocation: Decentralized versus Hierarchical Firms[J]. Journal of Finance, 2002, 57(5):1891-1921.

[7]Lin M, Prabhala N R, Viswanathan S. Judging Borrowers by the Company They Keep: Friendship Networks and Information Asymmetry in Online Peer-to-Peer Lending[M]// Judging Borrowers By The Company They Keep 1 : Social Networks and Adverse Selection in Online Peer-to-Peer Lending. 2013.

[8]Pope D G, Sydnor J R. What's in a Picture? Evidence of Discrimination from Prosper.com[J]. Social Science Electronic Publishing, 2011, 46(1):53-92.

[9]Emekter R, Tu Y, Jirasakuldech B, et al. Evaluating credit risk and loan performance in online Peer-to-Peer (P2P) lending[J]. Applied Economics, 2015, 47(1):54-70.

[10]PURO, Lauri, TEICH, et al. Borrower Decision Aid for people-to-people lending[J]. Decision Support Systems, 2010, 49(1):52-60.

[11]Burtch G, Ghose A, Wattal S. Cultural Differences and Geography as Determinants of Online Pro-Social Lending[J]. Mis Quarterly, 2014, 38(3): 773-794.

[12]Zhang J, Liu P. Rational Herding in Microloan Markets[J]. Management Science, 2012, 58(5):892-912.

[13]Berkovich E. Search and herding effects in peer-to-peer lending: evidence from prosper.com[J]. Annals of Finance, 2011, 7(3):389-405.

[14]Lee E, Lee B. Herding behavior in online P2P lending: An empirical investigation[J]. Electronic Commerce Research & Applications, 2012, 11(5):495-503.

[15]NANNI L,LU MINI A .An experimental comparison of ensemble classifiers for bankruptcy prediction and credit scoring [J] .Expert Systems with Applications, 2009, 36(2): 3028-3033.

[16]ABELL Á N J,CASTELLANO J G . A comparative study on base classifiers in ensemble method for credit scoring [J]. Expert Systems with Applications,2016, 73: 1-10.

[17]FLOREZ-LOPEZ R,RAM ON-JERONIM O J M . Enhancing accuracy and interpretability of ensemble strategies in credit risk assessment: a correlated-adjusted decision forest proposal [J].Expert Systems with Applications, 2015,42(13):5737-5753.

[18]TSAI C F, HSU Y F,YEN D C .A comparative study of classifier ensembles for bankruptcy prediction [J].Applied Soft Computing, 2014,24: 977-984.

[19]Cao Wei, Li Can, He Tingting , et al. Comparative study on credit risk early-warning models of P2P online lending in China based on integrated learning [J]. Data analysis and knowledge discovery, 2018,2(10):65-76.

[20]HOANG D T,KANG H J.A survey on deep learning based bearing fault diagnosis[J].Neurocomputing,2019, 335:327 -335.

[21]HINTON G E,SALAKHUTDINOV R R.Reducing the dimensionality of data with neural networks [J].Science,2006,313(5786):504 -507.

[22]Wang Lihua, Xie Yangyang, Zhang Yonghong, et al. Fault Diagnosis Method for Asynchronous Motor Based on Deep Learning [J]. Journal of Xi 'an Jiaotong University.2017, 5 1(10):128 -134.

[23]Zhou Qicai, Shen Hehong, Zhao Jiong, et al. Bearing Fault Diagnosis Based on Improved Stacked Cyclic Neural Network [J]. Journal of Tongji University (Natural Science edition),2019,47(10):1500 -1507.

[24]Yang Liusong, HE Guangyu. SVM Fault Diagnosis Method Based on Improved Particle Swarm Optimization [J]. Computer Engineering,2013,39(3):187 -190, 196.

[25]Hou Pingzhi, Zhang Ming, Xu Xiaobin, et al. Fault Diagnosis Method based on K-nearest Neighbor Evidence Fusion [J]. Control and Decision,2017,32(10):1767 - 1774.

[26]Yan Renwu, Ye Xiaozhou, Zhou Li. Fault Diagnosis technology of Power Electronic Circuit based on Random forest [J]. Journal of Wuhan University (Engineering Science), 2013,46(6):742 -746.

[27]Jiang Shaofei, Wu Tianji, Peng Xiang, et al. Data Driven Fault Diagnosis Method based on XGBoost Feature Extraction [J]. China Mechanical Engineering,2020, 31(10):1232 -1239.

[28]KE G L,MENG Q,FINLEY T,et al. LightGBM:a highly efficient gradient boosting decision tree [C]∥ Advances in Neural Information Processing Systems 30, New York:Curran Associates,2017.

[29]LIN M,CHEN Q,YAN S C.Network in network[J]. Computer Science,2013,arXiv:1312.4400.

[30]ZHANG W,PENG G L,LI C H,et al.A new deep learning model for fault diagnosis with good anti -noise and domain adaptation ability on raw vibration signals[J]. Sensors,2017,17(2):425.

[31]BREIM AN L .Arcing classifiers [J].The Annals of Statistics ,1998 ,26(3) :801-824.

[32]FREUND Y , SCHAPIRE R E . A decision-theoretic generalization of on-line learning and an application to boosting [J]. Journal of Computer and System Sciences , 1997 ,55(1) :119-139.

[33]KE G ,M ENG Q ,Finley T ,et al .Lightgbm :a highly efficient gradient boosting decision tree [C]//31st Conference on Advances in Neural Information Processing Systems .Long Beach ,CA :Neural Information Processing Systems Foundation ,2017 :3146-3154.