Economic Management & Global Business Studies invites you to contribute to the frontier of knowledge across disciplines and share your research with a global audience of peers and enthusiasts alike

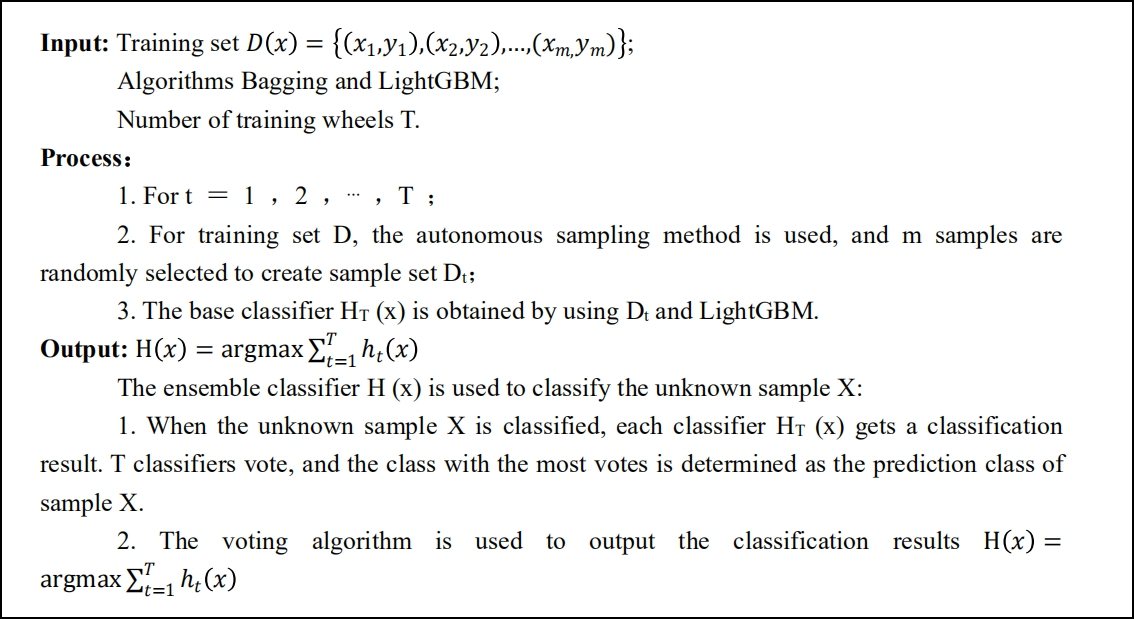

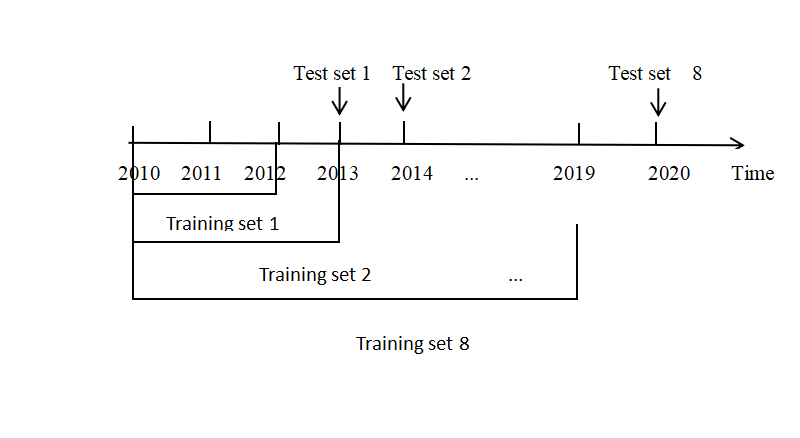

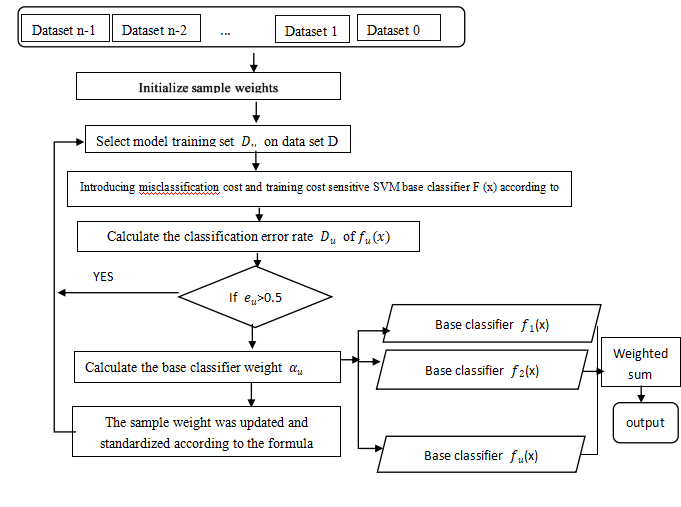

Research Objectives: Build a dynamic imbalanced financial distress prediction model to solve concept drift I and imbalanced data distribution simultaneously. Research Methods: Based on the improved AdaBoost algorithm, ADA-CSSVM-TW model is built with cost sensitive support vector machine as the base classifier, and the data of Chinese manufacturing companies from 2010 to 2020 are used for the empirical analysis. Research Findings: The ADACSSVM-TW model I can significantly improve the prediction accuracy, with excellent performance and reliable robustness. Research Innovations: The cost sensitive support vector machine is used as the base classifier of the improved AdaBoost algorithm, and the dynamic imbalanced financial distress prediction model is built. Research Value: The research of this paper has important theoretical value and practical significance for Chinese listed companies to effectively prevent the occurrence of financial distress in practice.

Al-Faraj, H., Wang, C., Yi-Jun, L., & Da-Wei, C. (2023). Dynamic Imbalanced Financial Distress Prediction Model Based on Improved AdaBoost Algorithm. Economic Management & Global Business Studies, 2(1), 2. doi:10.xxxx/xxxxxx

ACS Style

Al-Faraj, H.; Wang, C.; Yi-Jun, L.; Da-Wei, C. Dynamic Imbalanced Financial Distress Prediction Model Based on Improved AdaBoost Algorithm. Economic Management & Global Business Studies, 2023, 2, 2. doi:10.xxxx/xxxxxx

AMA Style

Al-Faraj H., Wang C., Yi-Jun L. et al.. Dynamic Imbalanced Financial Distress Prediction Model Based on Improved AdaBoost Algorithm. Economic Management & Global Business Studies; 2023, 2(1):2. doi:10.xxxx/xxxxxx

Chicago/Turabian Style

Al-Faraj, Hamza; Wang, Chenguang; Yi-Jun, Lin; Da-Wei, Chen 2023. "Dynamic Imbalanced Financial Distress Prediction Model Based on Improved AdaBoost Algorithm" Economic Management & Global Business Studies 2, no.1:2. doi:10.xxxx/xxxxxx

Al-Faraj, H.; Wang, C.; Yi-Jun, L.; Da-Wei, C. Dynamic Imbalanced Financial Distress Prediction Model Based on Improved AdaBoost Algorithm. Economic Management & Global Business Studies, 2023, 2, 2. doi:10.xxxx/xxxxxx

AMA Style

Al-Faraj H., Wang C., Yi-Jun L. et al.. Dynamic Imbalanced Financial Distress Prediction Model Based on Improved AdaBoost Algorithm. Economic Management & Global Business Studies; 2023, 2(1):2. doi:10.xxxx/xxxxxx

Chicago/Turabian Style

Al-Faraj, Hamza; Wang, Chenguang; Yi-Jun, Lin; Da-Wei, Chen 2023. "Dynamic Imbalanced Financial Distress Prediction Model Based on Improved AdaBoost Algorithm" Economic Management & Global Business Studies 2, no.1:2. doi:10.xxxx/xxxxxx

APA style

Al-Faraj, H., Wang, C., Yi-Jun, L., & Da-Wei, C. (2023). Dynamic Imbalanced Financial Distress Prediction Model Based on Improved AdaBoost Algorithm. Economic Management & Global Business Studies, 2(1), 2. doi:10.xxxx/xxxxxx

Article Metrics

Article Access Statistics

References

[1]Fitzpatrick P. J. , 1932, A Com parison of Ratios of Successful Industrial Enterprises with Those of Failed Firms [M], New York: Certified Public Accountant.

[2]Beaver W. H. , 1966, Financial Ratios as Predictors of Failure [J], Journal of Accounting Research, 4, 71~111.

[3] Altman E. I. , 1968, Financial Ratios, Discriminant Analysis and the Prediction of Cor porate Bankruptcy [J], Journal of Finance, 23 (4), 589~ 609.

[4]MselmiN., Lahiani A. , Hamza т. , 2017, Financial Distress Prediction: The Case of French Small and Medium-sized Firms [J], International Review of Financial Analysis, 50, 67~ 80.

[5]Kim S. Y., Upneja A. , 2014, Predicting Restaurant Financial Distress Using Decision Tree and AdaBoosted Decision Tree Models [J, Economic Modelling, 36, 354~362.

[6]Gogas P. , Papadimitriou T. , Agrapetidou A. , 2018, Forecasting Bank Failures and Stress Testing: A Machine Learning Approach [J], International Journal of Forecasting, 34 (4), 440~455.

[7] Moscatelli M. , Parlapiano F. , Narizzano s , Viggiano G. , 2020, Corporate Default Forecasting with Machine Learning [J], Expert Systems with Applications, 161, 113~167.

[8]Chawla N. V. , Bowyer K. W. , HallL. 0. , Kegelmeyer W. P. , 2002, SMOTE: Synthetic Minority Over-sampling Technique [J], Journal of Artificial Intelligence Research, 16, 321~ 357.

[9] Ganguly S. , Sadaoui S , 2017, Classification of Imbalanced Auction Fraud Data [J], Canadian Conference on Artificial Intelligence, Advances in Artificial Intelligence, 84~ 89.

[10]Freund Y. , Schapire R. E. , 1997, A Decision-Theoretic Generalization of On-Line Learning and an Application to Boosting [J], Journal of Computer and System Sciences, 55 (1), 119~139.

[11]Sahin Y. , Bulkan s , Duman E. , 2013, A Cost-sensitive Decision Tree Approach for Fraud Detection [J], Expert Systems with A pplications, 40 (15), 5916~ 5923.

[12] Tao X. M., Li Q ,Guo W. J., Ren C., Li C. х., LiuR. , Zou J. R. , 2019, Self-adaptive Cost Weights-based Support Vector Machine Cost-sensitive Ensemble for Imbalanced Data Classification [J], Information Sciences, 487, 31~56.

[13]Hulten G. , Spencer L. , Domingos P. , 2001, Mining Time-Changing Data Streams [CJ, Preceeding of the Seventh ACM SIGKDD, International Conference on Knowledge Discovery and Data Mining , 97~106.

[14]Koychev L. , 2000, Gradual Forgetting for Ada ptation to Concept Drift [с], Proceeding of the ECAI 2000 Workshop Current Issues in Spatio- Temporal Reasoning, 101 ~ 106.

[15] Almeida P. R. L. , OliveiraL. S. , BrittoJrA. S , Sabourin R. , 2018, Ada pting Dynamic Classifier Selection for Concept Drift [J], Expert Systems with Applications, 104, 67~ 85.

[16]Tölö E., 2020, Predicting Systemic Financial Crises with Recurrent Neural Networks [J], Journal of Financial Stability, 49, 100~ 146.

[17]Sun J., Li H. , Adeli H. , 2013, Concept Drift-Oriented Adaptive and Dynamic Support Vector Machine Ensemble with Time Window in Corporate Financial Risk Prediction [J], IEEE Transactions on Systems,Man, and Cybernetics. , 43 (4), 801~813.

[18]Sun J., Fujita H., ChenP., Li H. , 2017, Dynamic Financial Distress Prediction with Concept Drift Based on Time Weighting Combined with Adaboost Sup port Vector Machine Ensemble [J], Knowledge-Based Systems, 120, 4~14.

[19]Sun J. , Li H. , Fujita H. , Fu B. B. , Ai W. G. , 2020, Class-imbal anced Dynamic Financial Distress Prediction Based on Adaboost-SVM Ensemble Combined with SMOTE and Time Weighting [J], Information Fusion, 54, 128~144.

[20]BarddalJ. P. , Enembreck F. , Gomes H. M. , Bifet A. , 2019, Boosting Decision Stumps for Dynamic Feature Selection on Data Streams [J], Information Systems, 83, 13~ 29.